1. Executive Summary

Data centres are the backbone of the digital economy and AI revolution. This is significantly driving demand for energy and materials. Most discussion focuses on global data centre electricity consumption, which is projected to roughly double from its 2024 level by 2030, driven by AI, cloud computing, and the exponential growth of data. [IEA, Electricity 2025] Yet energy consumption is only part of the story.

The industry has a material challenge it has barely begun to address. Each megawatt of new data centre capacity embeds approximately 60–75 tonnes of minerals and metals. [WEF/Kearney, 2025] Short replacement cycles of 3–5 years contribute to electronics being one of the fastest-growing sources of waste on the planet. [Global E-waste Monitor, 2024]

Circular economy strategies represent one of the most significant, underexploited opportunities for the sector — both for business value and environmental impacts. Increasing equipment lifetimes and material re-use through repair, refurbishment, remanufacturing, and recycling can be positive for both business and the environment. Circularity is not a constraint on the data centre industry's growth — it is a design principle that fits naturally with what the industry already values: modularity, replaceability, scalability, efficiency, and speed. The business case is real and quantifiable: structured refurbishment programmes for a volume of 10,000 retired servers can recover €10M or more annually. [CEDaCI/WeLOOP, 2020] Extending fleet lifecycles selectively avoids hundreds of millions in replacement capital expenditure.

The technology works. The circular market infrastructure is emerging. Google is sourcing 44% of components for managed builds from reused inventory; Microsoft is achieving 90.9% reuse and recycling of retired hardware. [Google, 2026] [Microsoft, 2025] Yet structural barriers — misaligned operational incentives, absence of total expenditure (TotEx) considerations and a lack of shared language — prevent circular practices from scaling further.

Now it is time to move from exceptional isolated solutions to circular ecosystems. The question is not whether circular data centre operations are possible — it is whether the industry will scale what works, collectively. The window to act is open now.

2. Introduction: A Market in Hypergrowth

2.1 Unprecedented scale and speed of data centre buildout

Installed inventory capacity has been growing between 7–20% annually in Europe and up to 40% in North America in recent years. Global data centre electricity consumption stood at approximately 415 TWh in 2024 and is projected to reach around 945 TWh by 2030, roughly doubling over that period. [IEA, Electricity 2025] North America, Europe, and Asia Pacific dominate the market, but investment is accelerating across every region. [CBRE, 2025]

Sources: IEA, Electricity 2025; WEF/Kearney, 2025; CBRE, 2025.

This growth is driven by a fundamental shift in computing demand. The rise of generative AI has created a step-change in the power density required per rack, from a typical 5–10 kW for conventional servers to 50–100 kW or more for GPU clusters. [IEA, 2025] Major data centre operators are committing to multi-billion dollar infrastructure programmes that will define the physical geography of digital infrastructure for decades.

The impact on the hardware market is dramatic: the mere announcement of large-scale buildout plans can drive prices for RAM and other components to unprecedented levels, as market participants anticipate supply constraints and place forward bets on tightening availability. These expectations are not unfounded. The global RAM market is highly concentrated, with approximately 90% controlled by just three manufacturers, while production capacity remains difficult to scale and the cost of building new fabrication facilities exceeds USD 10 billion. [Net Valuator] As a result, prices are likely to continue rising. [Tom's Guide]

2.2 Technology racing ahead of deployment

What makes this buildout unusual is not just its scale but its speed relative to technological change. GPU chip architectures are refreshed on 12–18 month cycles. Cooling requirements for AI racks have shifted from air-based to liquid-based systems faster than most facility designers anticipated. This creates a structural tension: investors and operators are under pressure to deploy capacity as fast as possible, while the facilities they are building need to remain viable assets for 25 years or more. Legacy data centres, however, are often not equipped to accommodate such rapid change. Their facility architectures and core infrastructure components are not always designed for adaptability across evolving scenarios, while the demands placed on data centres continue to shift alongside technological advancement.

There is an important distinction between two separate arenas of server deployment: hyperscale operators, such as Google, Amazon, Microsoft, Alibaba, and Meta, and conventional enterprise data centre operators. The latter typically procure equipment through OEMs such as Dell, Lenovo, HPE, or Inspur, relying on standardized, largely x86-based architectures built on Intel or AMD processors. These systems are designed for broad compatibility and repeatability across customers, with relatively fixed configurations and upgrade paths defined by vendor roadmaps.

Hyperscalers, by contrast, operate at a fundamentally different level of vertical integration. They increasingly collaborate directly with chip designers (e.g., NVIDIA, AMD) and original design manufacturers (ODMs) to develop highly customized hardware stacks tailored to specific workloads, particularly for AI and high-performance computing. This includes bespoke server architectures, accelerators, networking fabrics, and increasingly, facility-level integration (e.g., direct-to-chip liquid cooling). As a result, hyperscale environments can iterate more rapidly and optimize for performance and efficiency at scale, but they also face greater exposure to fast-moving technology cycles and infrastructure obsolescence.

2.3 A window of opportunity for circular design

The data centre industry's buildout is largely controlled by a few dozen major organisations. Design decisions made by this group today will shape the material composition, replaceability, and end-of-life profile of millions of tonnes of equipment over the next two decades. Once facilities are built and procurement frameworks are locked in, circular design becomes exponentially harder to retrofit. The case for acting now is both environmental and financial.

3. Three Material Sustainability Challenges

The sustainability discussion in the data centre industry is often focused on energy efficiency in operations. In the current hypergrowth mode, substantial challenges related to embodied carbon, material supply chains, and component lifetimes need to be resolved to make the data centre industry future proof.

3.1 The climate challenge

Data centres currently consume approximately 1–2% of global electricity, rising rapidly. [IEA, 2025] Operational energy has historically dominated the industry's carbon footprint, accounting for up to 80% of whole-life emissions. Hence leading tech companies are signing power purchase agreements (PPAs) to secure clean energy supply for their data centres (for example Google). [Google] As grids decarbonise, the carbon calculus changes fundamentally. [Arup, 2024]

At the same time, embodied carbon — the emissions associated with the production, transportation, and installation of physical infrastructure and equipment — becomes an increasingly significant share of total lifecycle impact. [GHG Protocol] Most data centre carbon assessments exclude servers and storage entirely, treating them as tenant property. When they are included — alongside the fact that servers are replaced every 3–5 years over a facility's 60-year lifetime — the picture shifts fundamentally.

Source: Arup, Circular Thinking for Data Centres (2024); CEDaCI/WeLOOP (2020).

3.2 The critical materials challenge

Data centre equipment is built from a concentration of strategically important materials. The European Commission classifies many of the required materials as critical and strategic (CRMs). [EU CRMA, 2024]

| Material | Found in | Primary producers (top 3) | Refinery producers (top 3) | EU EOL-RIR* |

|---|---|---|---|---|

| Cobalt (Co) | Motherboard, PSU, LIB battery (UPS), HDD |

|

| 22% |

| Neodymium / REE | HDD motors, cooling fans, generators, UPS |

|

| 1% |

| Platinum group metals | Server (PCB), HDD, SSD, Motherboard, Network switch |

| — | 30% |

| Gallium (Ga) | CPU, PSU, VRMs/GPU cards |

|

| 0% |

| Lithium (Li) | LIB battery (UPS) |

|

| 0% |

| Aluminium | Heat sinks, rack chassis, cold plates, cable mgmt. |

|

| 21% |

| Copper | Cable & wiring, Server (PCB), transformers, motors, connectors |

|

| 30% |

| Germanium | Fiber optic transceivers, GPUs, SiGe chips | (by-product dominated) |

| 2% |

| Graphite | Batteries (UPS), thermal management |

| — | 3% |

| Nickel | Electroplating and connector coatings, PCBs, resistors, capacitors |

|

| 16% |

| Silicon metal (Si) | CPU, GPU, SSD, RAM, power semiconductors |

|

| — |

| Tantalum (Ta) | Server (PCB), Motherboard, RAM, Network switch |

| — | 13% |

| Tin | PCBs, capacitors, thermal interfaces |

|

| 11% |

| Indium (In) | CPU, displays, touchscreens, thermal interface material | (by-product of zinc production) |

| 0% |

| Gold (Au) | Server (PCB), Motherboard, CPU, Network switch |

|

| 24% |

| Silver | Server (PCB), Switches, PDUs |

| — | 19% |

*EOL-RIR: End-of-life Recycling Input Rate. Sources: EU CRMA (2024); EU RMIS.

Europe is almost entirely import-dependent for these materials, with structural dependency especially pronounced on China. The Critical Raw Materials Act (2024) sets targets of 10% domestic extraction, 40% processing, and 25% recycling by 2030. [EU CRMA, 2024] But currently, EOL-RIRs are structurally low in the EU.

The supply risks are not hypothetical. Gallium and germanium experienced price spikes of 25–30% following Chinese export restrictions in 2023–2024. [WEF/Kearney, 2025] Copper faces a projected 25–30% global shortfall by 2035. [WEF/Kearney, 2025]

3.3 The lifetime and obsolescence challenge

Servers, storage devices, and network switches are typically replaced every 3–5 years, driven not by physical failure but by performance obsolescence, energy efficiency improvements, or warranty expiry. [CEDaCI/WeLOOP, 2020] Reuse rates vary sharply: hard disk drives reach approximately 48% and memory cards approximately 40%, while CPUs are reused in only approximately 5% of cases and main circuit boards in just 3%. [JRC, 2015] Google's 2026 report: 44% of components for Google-managed server builds (not including OEM-managed builds) were sourced from reused inventory in 2024. [Google, 2026]

The financial cost of low reuse is considerable. A typical 3–4 year old enterprise server can sell for €2,000–8,000 on the refurbished market, compared to €12,000–25,000 new, with scrap value of just €15–22 per unit. [CEDaCI/WeLOOP, 2020] OEMs frequently limit firmware updates to authorised service channels, suppressing reuse rates [JRC, 2015] and driving premature disposal of functional hardware, contributing to more than 60 million tonnes of electronic waste per year. [Global E-waste Monitor, 2024]

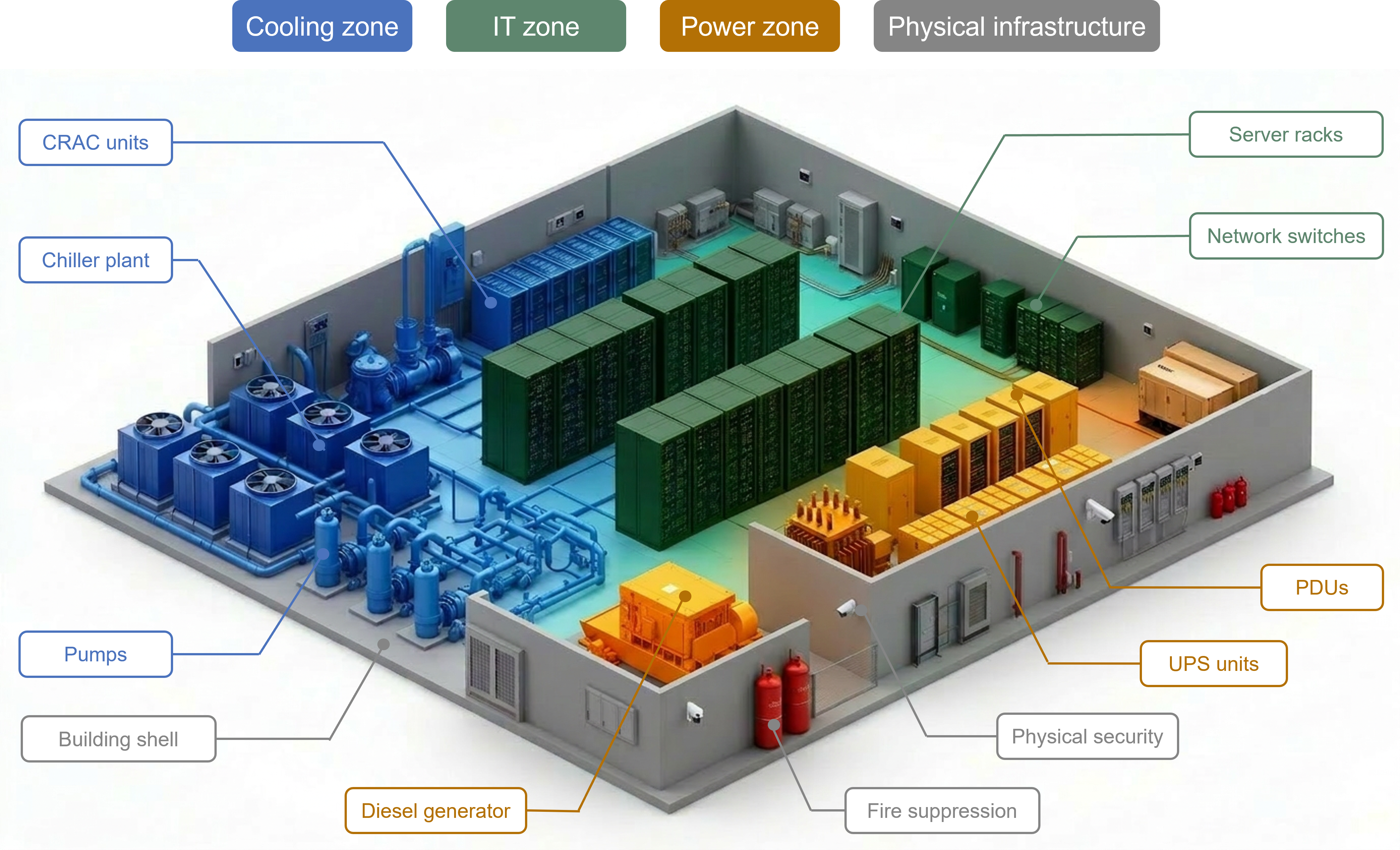

4. Data Centre Infrastructure and its Circular Potential

A data centre is an assembly of four functional zones — power infrastructure, IT equipment, cooling systems, and physical structure — each with a distinct material profile, replacement cycle, and circular economy relevance.

Power zone — how power is delivered reliably from the grid to the IT equipment

Electrical infrastructure delivers stable power from the utility to the IT equipment. Electricity enters the facility through service entrance switchgear, where it is protected and controlled, and is then stepped down via transformers. Power is distributed through switchboards and Power Distribution Units (PDUs), and ultimately delivered to server racks via rack-level power distribution. To ensure continuous operation, Uninterruptible Power Supply (UPS) units provide instantaneous backup power using batteries, preventing any interruption to IT systems. For longer outages, diesel generators supply sustained backup power. System resilience is achieved through redundant architectures (e.g., N+1, 2N), where multiple independent power paths and components ensure high availability.

IT zone — where compute, storage, and networking functions are performed

The IT zone contains the core computing infrastructure, including servers, storage systems, and networking equipment, typically housed within racks. Servers may be based on standardised architectures (e.g., x86 platforms from OEMs) or highly customised designs in hyperscale environments, often incorporating accelerators such as GPUs or specialised AI chips. Networking equipment (switches, routers) enables high-speed data exchange both within the data centre and externally. The IT zone is the primary consumer of both power and cooling, and its design directly influences infrastructure requirements in the other zones.

Cooling zone — how heat generated by IT equipment is managed and removed

Cooling systems manage the significant heat generated by IT equipment. Chilled water produced by the chiller plant is circulated via pumps to cooling units within the data hall. Computer Room Air Conditioners (CRAC) distribute cooled air to the server racks, while hot air is removed and returned for re-cooling, typically organised using hot aisle / cold aisle configurations. For higher-density workloads, particularly AI and HPC, liquid cooling technologies are increasingly deployed — including rear-door heat exchangers, direct-to-chip cooling, and immersion cooling. These require Cooling Distribution Units (CDUs) to manage fluid circulation and integration with facility-level systems such as cooling towers or dry coolers. Some facilities also use free cooling (air-side or water-side economisation), leveraging ambient conditions to reduce reliance on mechanical cooling.

Schematic representation of data centre infrastructure. Source: AI supported image created by authors.

Two concepts of "lifetime" are key. The technical lifetime is how long a component can physically keep operating with normal maintenance. The replacement cycle is how soon operators actually replace it — driven by performance upgrades, efficiency gains, warranty expiry, or perceived risk rather than physical failure. For many components, especially in the IT zone, these two numbers diverge sharply: a server replaced at 4 years may be physically capable of running for 10–15 years; a rack chassis retired alongside its servers may have 15 more years of structural life. This gap is where the circular economy opportunity arises.

Bubbles show typical replacement cycles as practised today, not technical lifetimes. Sources: Uptime Institute (2025); Procurri; CEDaCI/WeLOOP (2020).

5. The Circular Economy Opportunity

The data centre industry's high asset concentration, well-defined product categories, large equipment volumes, and small number of dominant operators create conditions highly favourable for systematic circular economy implementation, both for hyperscale as well as enterprise data centre buildout. There are five principal circular business levers.

| Component | Reduce design for less | Reuse redeployment | Refurbish / Remanufacture restore to spec | Recycle material recovery | Outcome models leasing / as-a-service |

|---|---|---|---|---|---|

| Power zone | |||||

| Batteries (UPS) | Medium | Low | Medium | Highcobalt & lithium recovery viable | Medium |

| UPS systems | Low | Low | Highlong-lived, repairable units | Low | Highplant leasing established |

| PDU + switchgear | Low | Medium | Highmodular, long service life | Low | Medium |

| IT zone | |||||

| Servers (rack / blade / GPU) | Highrecycled Al, modular — proven at hyperscale | Highlarge secondary market exists | HighOEM take-back available | Highgold & silver drive economics | HighGPU-as-a-service growing |

| Storage — HDD | Medium | Highhigh residual value if sanitised | Highdata wipe enables redeployment | Hightargeted CRM recovery proven | Low |

| Storage — SSD | Medium | Medium | Medium | Medium | Low |

| Network switches | Medium | Medium | Highvendor programmes exist | Highcircuit board-rich, gold content | Medium |

| Racks + chassis | Medium | High10–15yr life, often wasted | Medium | Medium | Low |

| Cooling zone | |||||

| Chillers | Low | Low | Highhigh-value, serviceable plant | Low | Highcooling-as-a-service |

| Refrigerant | Highswitch to low-GWP type | — | Medium | Medium | — |

| Liquid / immersion cooling | Medium | Low | Highfluid regeneration viable | Low | Highleasing model natural fit |

| Physical infrastructure | |||||

| Building structure | Highlow-carbon concrete & timber | Medium | Medium | Medium | — |

Sources: CEDaCI/WeLOOP (2020); Google (2026); authors' assessment.

5.1 Reduce material and cost — product design and material choice

Top opportunity: switching to lower-impact refrigerants and low-carbon building materials; designing for adaptability rather than a specific technology generation.

Reduction means designing out material intensity before equipment is manufactured. Switching from high-GWP refrigerants to lower-impact alternatives can reduce refrigerant-related lifecycle climate impact by around 60–80%. Building material choices — low-carbon concrete mixes, structural timber alternatives and recycled materials — are already being deployed by several major operators.

In the IT and cooling zones, the practical strategy is designing for adaptability: modular power distribution, cooling systems designed for zonal expansion, and floor layouts that preserve flexibility. At the server level, Google has demonstrated that heatsinks in one of its server tray designs now consist of 100% recycled aluminium. [Google, 2026] This represents the frontier of current practice, not the industry norm.

Beyond this, advanced data analytics and predictive intelligence could help reduce redundancy requirements over time. Redundancy is designed to enhance operational resilience and typically involves additional equipment — such as extra chillers, duplicate power paths, standby generators, and UPS batteries. These assets are generally sized for peak load conditions but spend most of their operational life either idle or underutilized.

While such redundancy is critical for mitigating risks — such as equipment failure, heat-induced performance degradation, or data loss — it also introduces opportunities to improve resource efficiency. Emerging approaches could include dynamic, software-defined redundancy models that adapt capacity in real time, more integrated coordination with energy grids and demand-response systems, or even shared redundancy architectures across multiple facilities.

Siemens — building circularity into the data centre ecosystem

Siemens connects design, construction, and operations through a Digital Thread. Digital Twin technology enables energy flow simulation before construction begins. AI-enhanced cooling optimisation software reduces cooling energy use. [Siemens]

Circular principles driving impact

- Reduce — operations: AI-based White Space Cooling Optimization delivers up to ~40% cooling energy savings alongside 5–10% PUE improvement.

- Reduce — design stage: Digital Twin embeds efficiency before procurement is locked in.

- Prolong lifetime: Predictive maintenance extends infrastructure asset life.

Schneider Electric — a designated circularity model for data centre infrastructure

Schneider Electric's circularity model spans design, manufacture, deployment, operation, upgrade, and end of life. The EcoFit programme extends the operating life of installed power infrastructure through AI-powered diagnostics and targeted component upgrades.

Circular principles driving impact

- Reduce: Committed to 50% green material content in products by 2025. [Schneider Electric]

- Prolong lifetime: EcoFit extends asset life by up to 25% while reducing lifecycle carbon.

- Reuse: Take-back programme and end-of-life refurbishment.

5.2 Retain value through reuse and refurbishment — prolong equipment lifetime

Top opportunity: servers, hard drives, and racks — the secondary market exists and is growing, but captures only a fraction of the available value.

Extending the operational life of servers from typical refresh cycles (3–5 years to 6–7 years) can reduce annualised embodied carbon emissions by an estimated 30–40%. A critical enabler is data sanitisation and a transparent chain of custody: software-based data wiping preserves the reuse potential of storage devices entirely. For the majority of commercial data classifications under GDPR, software-based wiping is fully compliant. [ENISA] [NIST SP 800-88] The Circular Drive Initiative (CDI) is a global partnership advancing the secure reuse of storage hardware to reduce electronic waste across the data-centre ecosystem.

Eco-labels such as the latest generation of EPEAT already require data sanitisation capabilities as a mandatory criterion to enable circular business models. These practices are further incentivised through additional certification credits when such procedures are made publicly available. [EPEAT SUR 2025] While EPEAT certification is not generally mandatory, it is increasingly used as a procurement requirement by major enterprise purchasers; for servers, active EPEAT-registered OEMs currently include Cisco, Dell EMC, Fujitsu/FSAS, HPE, Lenovo, Supermicro, and xFusion.

When equipment is procured through distributors, a disconnect often arises between OEMs and operators, as manufacturers lose visibility over the location and usage of their products. This lack of traceability creates significant barriers to effective take-back, refurbishment, and remanufacturing programmes, as it becomes more difficult to identify, recover, and reintegrate equipment into circular value chains.

Hyperscale operators manage their own infrastructure build, reuse, and refurbishment strategies, as their equipment is typically highly customised and largely incompatible with both other hyperscale systems and standard enterprise hardware.

Google — hardware harvesting, lifetime extension, and closing the reporting gap

Google's March 2026 report, Bridging the Gap: Operationalising Circularity in Data Centers, documents operational achievements and structural challenges. Google's reverse supply chain: internal reuse first, then secondary market remarketing, then recycling as a last resort.

Circular principles driving impact

- Internal reuse at scale: 44% of components for Google-managed server builds (excl. OEM-managed) sourced from reused inventory in 2024.

- Component harvesting: 8.8M components harvested; 6.7M resold into secondary markets; 3M+ hard drives securely wiped and reused (2024).

- CRM recovery ("Mining the Cloud"): Non-functional hardware stripped of critical raw materials — including neodymium magnets — before any bulk shredding.

- Bridging the reporting gap: Google identified the "aggregation problem" and "value disconnect" as structural barriers.

Microsoft Circular Centers — reuse at hyperscale

Microsoft operates on-site Circular Centers at its hyperscale cloud data centres globally, processing end-of-life hardware through an AI-driven routing system directing each component to its highest-value pathway.

Circular principles driving impact

- Reuse at scale: 85% of demand for obsolete spare parts met from Circular Center inventory.

- Secondary market & recycling: 90.9% reuse and recycling rate for servers and components in 2024.

- Circular design feedback loop: Operational data fed back to equipment suppliers.

5.3 Increase resilience and reduce cost through remanufacturing

Top opportunity: servers, cooling plant, and dielectric fluids.

Remanufacturing — returning a product to original manufacturer specifications using a combination of recovered and new components — goes beyond simple refurbishment. Manufacturer-led programmes disassemble returned equipment to component level, reintegrate grade-A parts into new builds, certified refurbished units, or spare parts, and route the remainder to recycling. [Google, 2026]

Remanufacturing strategies are largely OEM or hyperscale operator specific, due to the lack of interoperability between the different hardware components.

A growing regeneration opportunity lies in the specialist fluids used in direct-to-chip or immersion cooling systems. Established purification processes restore them to as-good-as-new quality at 20–30% lower cost and 80% lower carbon emissions compared to replacement with virgin fluids. [Electrical Oil Services]

Retronix — recovering value from the AI hardware upgrade cycle

Retronix disassembles boards from refreshed AI infrastructure, tests and certifies individual components to industry standards, and redeploys them to edge computing, backup systems, or development environments. [Retronix, 2024]

Circular principles driving impact

- Cascading reuse: ~2.5 million components recovered annually, $5M value recovered via reuse.

- Supply chain resilience: Certified secondary inventory buffers against semiconductor lead times.

5.4 Reclaim value through recycling — keep materials in the loop

Top opportunity: server circuit boards (gold and silver) and batteries (cobalt and lithium).

Circuit boards are the highest-value recycling stream: gold and silver content drives economics, while gallium, germanium, tantalum, platinum-group metals, and cobalt represent recoverable critical materials currently mostly lost. Effective recycling strategies depend largely on the availability of data regarding the concentration of recoverable materials within individual components. Sophisticated smelting and chemical recovery processes — exemplified by Umicore precious metals refining in Belgium — can recover gold, silver, copper, and palladium from circuit boards at scale. [Umicore] Johnson Matthey shows that recycled PGMs have a ~97% lower carbon intensity compared to primary mined metals. [Johnson Matthey] Google's "Mining the Cloud" programme systematically strips non-functional servers of critical raw materials — including neodymium magnets — before any bulk shredding. [Google, 2026]

Amazon Web Services — circularity embedded across the hardware lifecycle

AWS sources spare parts from its own reuse inventory, extends hard disk drive lifespans through predictive maintenance, and resells functional components at volume.

Circular principles driving impact

- Reuse at scale: 13% of spare parts from internal reuse inventory; 23.5 million components recycled or resold.

- Asset life extension: Hard drive lifespan extended by 2+ years through predictive analytics.

- Reduce — energy intensity: PUE typically ~1.15, vs industry average of ~1.63.

- Material circularity: 30% of plastic rack components now recycled or bio-based.

5.5 Create new revenues from outcome-based and leasing offerings

Top opportunity: cooling and power backup are the most mature use cases; GPU-as-a-service is the emerging IT frontier.

When manufacturers retain ownership and sell capacity or uptime rather than hardware, they have a direct financial interest in product longevity, repairability, and end-of-life recovery. GPU-as-a-service is beginning to decouple AI compute economics from physical hardware ownership. [Digital Ocean] [STL Partners]

Equinix — turning data centre waste heat into community energy

Equinix captures residual heat from its server halls and exports it to municipal district heating networks. The programme launched in Helsinki in 2010 and has since expanded to Paris, Frankfurt, Toronto, and other cities.

Circular principles driving impact

- Reuse (waste to resource): 14.5 GWh of heat exported in 2024.

- Community energy loops: Supplied heat to the 2024 Olympic pool complex and thousands of homes around Paris, Helsinki, and Frankfurt.

- Reduce: Each GWh exported displaces fossil fuel combustion in district heating networks.

6. What Needs to Change — and Who Must Act

The case studies above illustrate the frontier of what the industry has demonstrated is possible, and these results are impressive. It is now time to consolidate and spread these learnings across the entire industry to make sure that circularity levers become fundamental design criteria in the rapid scale-up — from leading practices to collective industry standards.

6.1 From CapEx and OpEx to Total Expenditure (TotEx)

Today, most data centre investment and operational decisions are governed by a separation between capital expenditure (CapEx) and operational expenditure (OpEx). While this distinction is useful for financial planning, it creates a structural barrier to circular economy implementation.

Circularity requires a Total Expenditure (TotEx) perspective, one that captures the full lifecycle cost and value of an asset, from procurement and operation to refurbishment, resale, and material recovery. Decisions that appear cost-efficient under a CapEx or OpEx lens may destroy value when viewed across the full lifecycle.

For example, prematurely replacing a functional server may optimise short-term performance metrics but forgo residual value, increase embodied carbon, and trigger unnecessary reinvestment. Conversely, extending asset lifetimes or enabling secondary use cases may reduce total cost of ownership while improving sustainability outcomes.

Moving towards a TotEx mindset requires breaking down internal cost silos and aligning incentives across procurement, operations, and sustainability functions within organisations.

6.2 The organisational barriers

The hurdle for a more circular data centre industry is not only technical or financial. Successful circularity often requires a solid top-down mandate, clear organizational responsibility and breaking down silos and misaligned incentives across the organization. Google's 2026 analysis reveals two distinct organisational barriers. The first is the "value disconnect" — an incentives problem at the operational level. Data centre teams are evaluated on highly specific goals, such as uptime, speed of deployment, not on circularity outcomes, such as supply resilience and cost efficiency, which are incentives of the purchasing department. Careful component harvesting is slower than bulk scrapping and is perceived as friction against primary performance objectives. One way to incentivise these circular processes would be to introduce an internal cost for carbon emissions. However, the contribution of circularity to emission reductions is not easily quantified, due to the lack of widely accepted methodologies. A recent study involving 12 industry partners from the electronics sector has developed CBMI, a methodology designed to make these impacts more reliable and comparable. [CBMI] As long as the KPIs that govern day-to-day work do not reward circular behaviour, that behaviour remains dependent on individual commitment rather than systemic design.

The second is the "aggregation problem" — a reporting and visibility problem at the corporate level. Even where circular work does happen, it disappears when reported upward, absorbed into generic metrics like "general task completion." Progress towards corporate sustainability goals cannot be demonstrated if the relevant operational data is never captured. These two barriers must be addressed separately: the value disconnect requires changing incentive structures and KPIs; the aggregation problem requires a shared language and unified reporting framework. [Google, Bridging the Gap, 2026]

"The value disconnect and the aggregation problem are as important as any technical gap — and they affect every organisation in the industry."Google, Bridging the Gap: Operationalising Circularity in Data Centers (2026)

These organisational barriers are not unique to Google. They illustrate the complexity of making circular approaches work in practice at company level, even for pioneering players. While these companies are paving a path and demonstrating feasibility, lifting the full circular potential and resolving the material challenges in the data centre industry will require systemic interventions from all industry stakeholders.

6.3 ⚙️ Circular data centres — enabled by design

The design phase already determines the full lifecycle performance and end-of-life outcomes. OEMs have strong leverage:

Firmware openness: In the past and still today, restricted firmware updates to authorised service channels has been suppressing reuse rates of critical components, such as processors, main circuit boards, and power supply units. Current EPEAT criteria require OEMs to provide access to firmware; [EPEAT SUR 2025] however, according to industry sources, full implementation of this requirement is not yet consistently realised in practice. Providing controlled access to firmware, diagnostics, and update tools for certified secondary market actors enables safe redeployment of components beyond primary use.

Design for disassembly: Replacing adhesive bonds and proprietary fixings with clip or lever systems; reducing the variety of plastic types used; designing for non-destructive, automated disassembly. Such design choices increase the ease of serviceability and automation and make the separation of high-value components feasible.

Data sharing: A key enabler of circular data centre ecosystems is the availability of reliable, standardised asset data across the lifecycle. Digital twins and digital product passports (DPPs) provide the foundation for this. By capturing information on material composition (e.g. critical raw material content), performance history, maintenance records, and ownership, these tools enable:

- performance optimisation during operation

- informed refurbishment and remanufacturing decisions

- transparent and trusted secondary market transactions

While policy frameworks such as ESPR are beginning to mandate product-level transparency, leading organisations can already adopt these tools proactively. [ESPR, 2024] EPEAT certification is also encouraging CRM disclosure for optional points. [EPEAT SUR 2025]

Calls to action — equipment manufacturers

- Share publicly which current product lines support firmware updates for secondary market buyers. This would send a significant market signal.

- Publish critical raw material content data for top 10 products by revenue, alongside carbon disclosures.

- Define an internal "circular design readiness" standard covering firmware openness, disassembly time, plastic type count, and material disclosure completeness.

- Offer take-back, certified refurbishment, or remanufacturing pathways for key categories — and make terms transparent so buyers can factor them into procurement decisions.

- Engage proactively in ESPR implementing acts for IT equipment to shape standards for DPPs that are practically implementable and maximise circular value.

6.4 🏢 Durability and lifetime productivity — operators must use their procurement power and govern asset value

A small number of operators control a large fraction of global purchasing decisions for data centre IT equipment. When operators make longevity part of their procurement criteria, they create the market conditions for manufacturers to invest in longer-lived, more maintainable products.

Hyperscalers have the most direct influence through procurement at scale. Their strongest levers are circular procurement clauses (firmware openness as an award criterion, CRM disclosure, take-back requirements), a formal decision gate at decommissioning so assets are classified for reuse or refurbishment rather than destruction by default, and separation of rack (and other component) lifecycles from server refresh cycles. Life extension must be workload-class specific and should be balanced against potential energy efficiency gains per unit of compute from equipment upgrades.

Colocation providers cannot directly control tenant IT refresh decisions; their strongest lever is in the building infrastructure, power and cooling zones: embedding maintainability, adaptability, lower-impact refrigerants, and modular cooling layouts into design briefs. Influence over tenants comes through sustainability disclosure requirements in lease terms.

Enterprise operators face internal governance and risk aversion that often push viable assets into premature replacement. The most practical intervention is segmenting the installed base by criticality and making the second-life decision path explicit in procurement and decommissioning governance.

As embodied carbon becomes a defining factor in data centre sustainability, operators need to move beyond purely financial decision frameworks. One practical approach is the introduction of internal carbon pricing at the asset level. This may enable more accurate comparisons between replacement, reuse, and refurbishment pathways and prevent premature asset retirement, and reduce the risk of stranded assets.

Beyond tracking individual assets, circular data centre operations require a system-level understanding of material flows. This implies moving towards material flow accounting, where organisations track the inflow, stock, and outflow of critical materials across their operations. By linking procurement data, asset inventories, and end-of-life outcomes, operators can create a dynamic "material account" that reflects both economic value and environmental impact.

Circularity at scale is fundamentally a data problem. Organisations cannot manage what they do not measure — and today, most data centre operators lack a comprehensive, asset-level view of material composition, lifecycle emissions, and residual value. Emerging standards and frameworks — such as the WBCSD Circular Transition Indicators and PACT 2.0 — provide a foundation for harmonised data collection and reporting. Over time, such systems will enable more transparent procurement, more efficient secondary markets, and more accurate corporate reporting. [PACT] [CTI Tool]

Calls to action — data centre operators

- Conduct an internal audit of current ITAD practice. What proportion of retired equipment undergoes physical destruction when software-based data deletion would be fully compliant? The answer quantifies the value currently being destroyed.

- Add three minimum requirements to server procurement briefs: firmware updates available for secondary market buyers; critical raw material content disclosure; and a take-back option at end of useful life.

- Build a digital inventory of assets and material flows, linked to lifecycle assessment (LCA) data across Scope 1–3 emissions. This includes tracking:

- material composition and critical raw material content

- operational performance and utilisation

- refurbishment potential and residual value

- end-of-life pathways and recovery outcomes

- Pilot a structured refurbishment programme with a qualified ITAD partner for at least one equipment category — for example, storage.

- Separate the lifecycle assumptions of servers, racks, and mechanical and electrical systems. Short IT refresh cycles should not pull longer-lived assets out of service prematurely.

- Integrate carbon-adjusted lifecycle costing into financial and operational decision-making.

- Demand performance-based and outcome-oriented contracts from key equipment and infrastructure suppliers, shifting commercial incentives toward long-term asset performance.

- Develop internal circular reporting frameworks — connecting operational circular activities to corporate sustainability metrics — to bridge the "aggregation problem" and make circular work count. Consider adopting shared frameworks such as the WBCSD Circular Transition Indicators to ensure cross-organisational comparability. [WBCSD CTI]

- Actively facilitate dialogue between hardware design, operations, and sustainability teams. Many circular practices already happen on the operations floor but are invisible to strategy — bridging that silo is as important as any new programme.

- Seek location opportunities with a high potential for integration into the wider energy and industrial ecosystem, e.g. renewable energy generation assets or district heating networks.

6.5 ♻️ Refurbishment excellence — the ecosystem needs to scale and standardise

Over 100 specialist brokers operate across North West Europe alone, and the refurbishment sector generates approximately $6.9bn in EU ICT turnover annually. [CEDaCI/WeLOOP, 2020] Equipment used by hyperscale operators is often highly customized and not easily compatible with secondary markets, and is typically not made available for resale. Hence the refurbishment market for data centre IT equipment mainly relies on hardware from enterprise data centre operators. But the market is fragmented, lacks common grading standards, and captures only a fraction of available value.

Refurbishment propositions are most effective when focused on specific high-potential asset categories, such as enterprise servers, storage, network switches, racks, and cooling plant, rather than generic end-of-life handling. Transparent reporting on value recovered, destruction avoided, and downstream treatment builds buyer trust and will increasingly become a competitive differentiator. Common grading standards for refurbished enterprise IT equipment would increase buyer confidence and market liquidity. And automation in dismantling, testing, repair/refurbishment could help scale capacity and lower costs.

Calls to action — ITAD operators and refurbishers

- Build propositions around specific high-potential asset categories rather than generic end-of-life handling.

- Develop transparent reporting on value recovery, avoided destruction, and downstream treatment of retired assets.

- Engage actively in EU standards development for grading and certification — the ESPR implementing acts are being written now.

- Explore forward-volume take-back agreements with operators that provide advance visibility of decommissioning timelines and enable capacity planning and utilization optimization, as well as matching with demand forecasts.

- Engage with industry platforms such as the Circular Electronics Partnership (CEP) or the Open Compute Project (OCP) to build the shared infrastructure and common language that a circular market requires.

6.6 🏛️ Supportive enabling conditions — policy must close the remaining gaps

ESPR implementing acts for IT equipment must include firmware openness, disassembly instructions and time targets, as well as CRM content disclosure in design requirements. [ESPR, 2024] Right-to-Repair for business contexts covering firmware access, spare parts, and service documentation would boost the independent remanufacturing ecosystem. Digital Product Passports (DPPs) for IT equipment would remove the information gap that currently suppresses secondary market prices. WEEE reform must introduce reuse as a separate, measurable target category. [WEEE Directive reform]

Calls to action — policymakers

- Ensure ESPR implementing acts for servers and network equipment include firmware openness, dismantlability scores and CRM disclosure requirements. Bring industry into consultation before requirements are finalised.

- Shape digital product passport requirements for IT equipment to reduce information asymmetry and permit automated dismantling, refurbishment and remanufacturing at scale.

- Introduce reuse as a separate, measurable target category in WEEE reform, distinct from and additional to recycling targets, with a clear trajectory to 2030.

- Extend Right-to-Repair provisions to business-to-business transactions in IT equipment, covering firmware, parts, and service documentation.

- Open Compute Projectopencompute.org/wiki/OCP_Sustainability_Initiative⭐Member companies in the OCP Sustainability group are also working on this topic — watch OCP for new insights to come

- Circular Drive Initiativecirculardrives.org

- Circular Electronics Partnershipcep2030.org

- Net Zero Data Centersnetzerodatacenters.com

7. Conclusion

The data centre industry is at an inflection point. It is deploying infrastructure at unprecedented scale — embedding 60–75 tonnes of minerals and metals per megawatt of new capacity [WEF/Kearney, 2025] — into a period of rapid technological change, with sustainability constraints tightening faster than most operators' planning cycles anticipate. The window of opportunity for embedding circular design principles is open, but it will not stay open indefinitely.

The case studies in this paper show that circular data centres are not a future ambition but a present possibility. Google sourcing 44% of Google-managed build components from reused inventory, Microsoft achieving 90.9% reuse and recycling of retired hardware, and AWS recycling or reselling 23.5 million components are real, documented achievements. Yet the value disconnect and the aggregation problem — misaligned operational incentives and invisible circular value in corporate reporting — are as important as any technical gap, and they affect every organisation in the industry. [Google, 2026]

The good news is that the levers are available and the business case is real. Refurbished servers command residual values far exceeding their scrap equivalent. Extending the useful life of a fraction of a large fleet avoids hundreds of millions in replacement capital expenditure. Structured critical component and material recovery reduces exposure to geopolitical supply shocks that are already materialising. And as regulatory pressure — ESPR, WEEE reform, Battery Regulation, Scope 3 reporting — moves consistently in one direction, early movers can now help shape the external conditions for this business opportunity.

What is needed: alignment on circular design choices and breaking current barriers collectively. Procurement requirements that signal demand to OEMs; design standards that enable circular flows at scale; policy frameworks that shift the economics of secondary markets; and the shared language and reporting infrastructure that allows circular value to move from the server floor to the boardroom.

Contact: paul.woebkenberg@circularity.me